How do I use a certificate of deposit?

Learn ways a CD can help you save

What is a CD?

A certificate of deposit is a low-risk savings option. It provides a guaranteed return1 and is federally insured up to $250,000 per account owner.

1. You can be charged an early withdrawal penalty if you take money out before a specified date. It’s important to review a CD’s terms carefully prior to opening one.

How does it work?

You deposit a specific amount of money for a set period of time, called the term. In return, the bank pays you interest. At the term’s end, you get your original deposit plus the earnings.

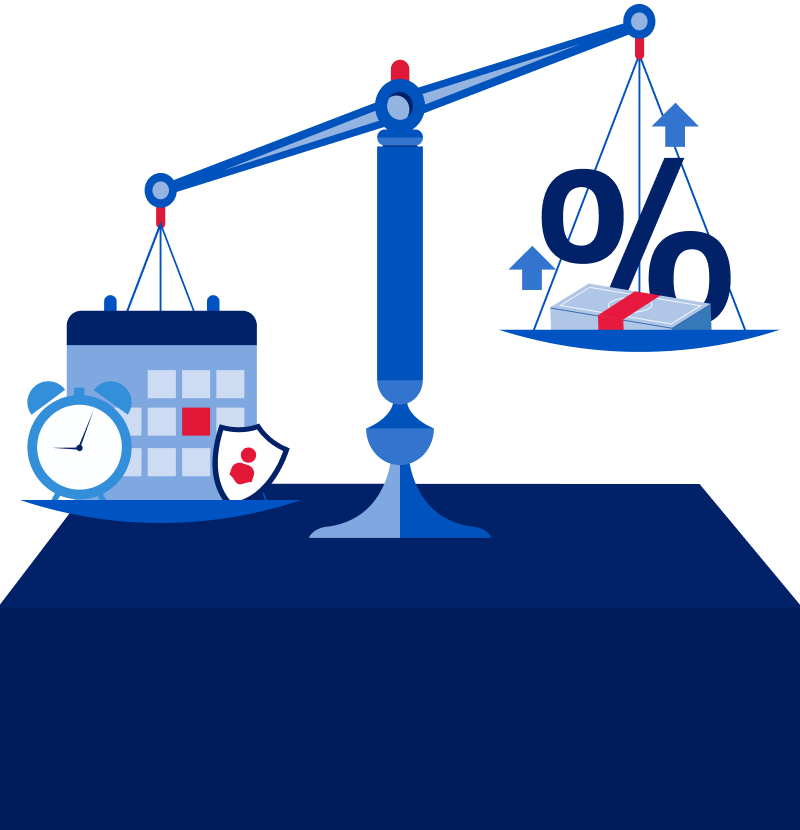

How are CD rates set?

CD interest rates depend on market conditions, amount deposited and term. They are usually higher than rates on savings accounts, but the money is less accessible.

What’s a CD good for?

A CD can be part of a diversified investment portfolio and works well for a goal that has a time element, such as:

How do I pick a CD?

Consider your goal, then shop around for a CD that balances term and return. A withdrawal penalty could apply if you take money out early, so review a CD’s terms carefully prior to opening.

How do I open a CD?

Go to your bank’s website or mobile app. You can also call or visit a branch. You’ll need to fill out an application and present identification.

What’s a CD ladder?

It's a popular strategy of putting money into CDs with different terms. It gives you easier access to funds as shorter-term CDs mature with the potential for higher returns depending on the rates locked in for the various CDs selected.

How do I build a CD ladder?

Divide your deposit among CDs of increasing terms—say one to three years. As a CD matures each year, continue the ladder by setting up a new three-year CD. Or you can use the cash for another purpose.

Did you know?

CD ladders help protect against changing market conditions. If interest rates fall, you’ve already locked in the higher rates. And if they rise, you can reinvest the maturing CD at the new rates.

You may also be interested in

This material is for informational use only and is not intended for financial or investment advice. Bank of America Corporation and/or its affiliates assume no liability for one’s reliance on the material provided. This material is not updated regularly and may not be current. Consult a financial professional when making financial decisions. ©2025 Bank of America Corporation.